Airline Industry Fundamentals and Current Trends

It is important to understand the current airline operating environment and the changes occurring within the airline industry. This information can provide context for the airport’s current air service situation and the difficulties of air service development today for all airports, both small and large. Several trends are discussed here including:

- Oligopoly: The domestic airline industry is comprised of four major airlines and a series of smaller ones.

- Hub and Spoke System: In an attempt to maximize customer access to its network, many airlines build hub and spoke systems. Hubs provide a connection point between origins and destinations.

- Service Changes: As the economic and financial requirements on airlines evolve, airline service patterns must evolve to ensure financial viability. Many times these service changes can negatively impact small and mid-sized markets.

- Aircraft Type: Technological advancements in aircraft capabilities and changes in consumer demand and airline economics have gradually driven a move toward larger and longer range aircraft.

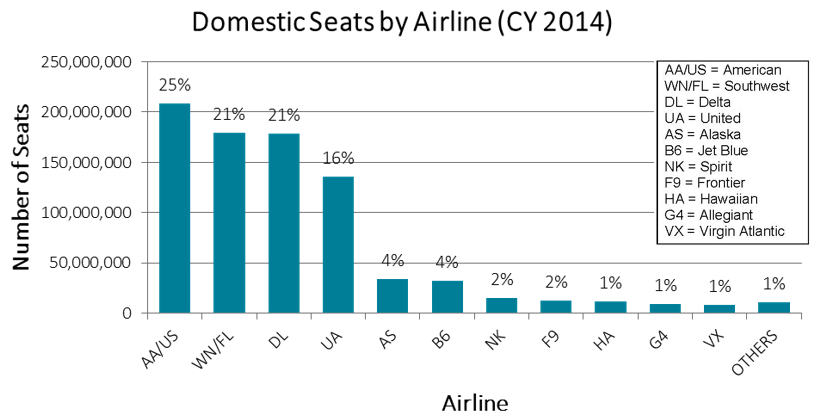

Today’s airline industry has evolved over time to a point where just four airlines control nearly 85 percent of the domestic U.S. market. The four airlines include: American Airlines (merged with US Airways), Delta Air Lines (merged with Northwest Airlines), United Airlines (merged with Continental Airlines) and Southwest Airlines (merged with AirTran Airways). The table below provides the number of seats each airline was scheduled to fly within the United States in calendar year 2014.

Source: Diio Mi Schedule

Source: Diio Mi Schedule

In recent years these four largest airlines have focused on international growth while their domestic U.S. systems have generally been stagnant or shrinking. Domestically, growth is being achieved through “addition by subtraction,” that is, for one market to gain new air service, another market must lose air service due to limited aircraft, regional airline pilot availability and other economic factors.

Three of the big four (American, Delta, and United) airlines (and to a lesser extent Alaska Airlines) operate their business model as a “hub-and-spoke” system, where a traveler going from point A to point B often “connects” at a hub airport en route to their final destination. Under this business model, service from many communities is funneled into one of the large “hub” cities and travelers must catch a connecting flight to their final destination. This demand aggregation model allows multiple airports to be connected via a single “hub” connecting airport. The other airlines such as Southwest Airlines operate under what is known as the ”point-to-point” model where service is operated in markets in which the traveler going from point A to point B does not have to make a connecting stop in order to make it to their final destination.

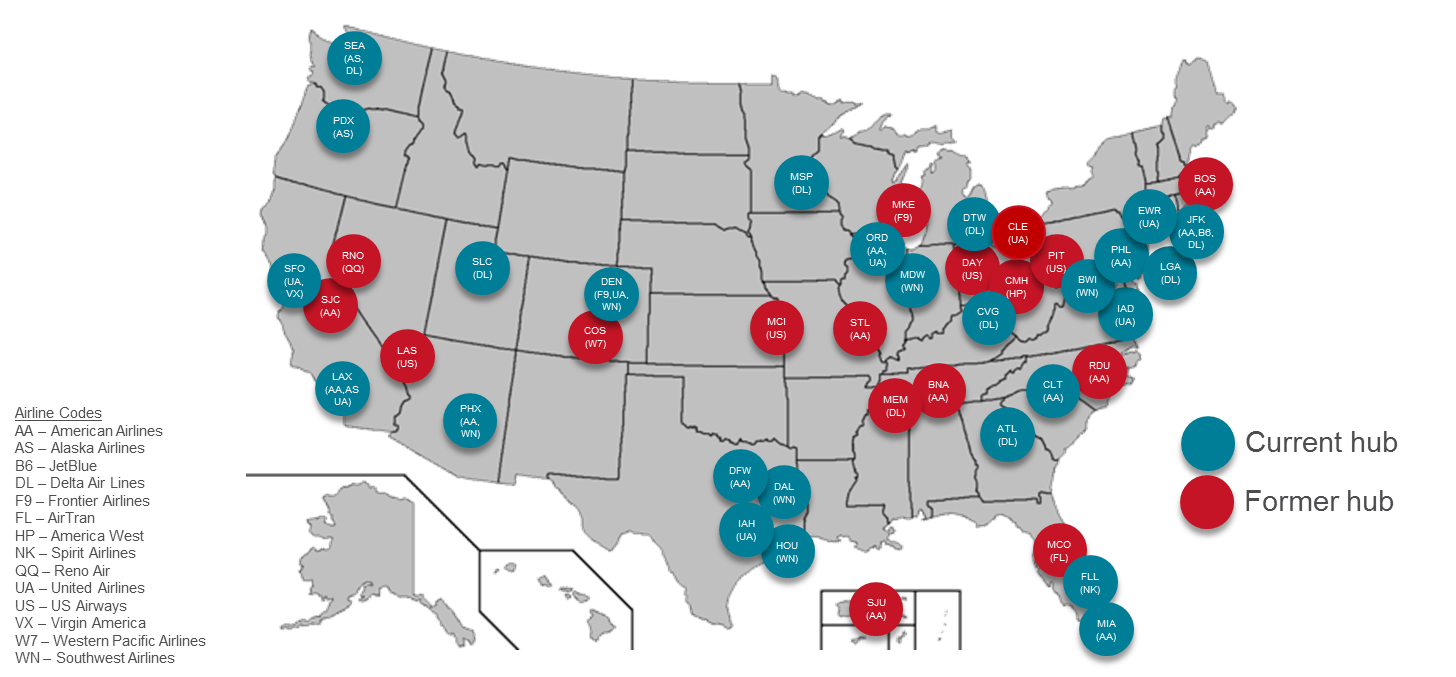

Current and Former Hubs/ Focus Cities (2000 – 2015)

Source: Mead & Hunt analysis / Diio Mi airline schedules

Source: Mead & Hunt analysis / Diio Mi airline schedules

One of the big benefits to the hub-and-spoke system is that service to many small communities that don’t have enough travelers to justify the economic investment for air service to many destinations can gain global access to the air transportation network by being a spoke airport that is funneled into one of the large hub airports. In order to economically operate these spoke services to smaller communities, the airlines that operate hubs contract with or use their owned regional (or feeder) airlines to provide the service.

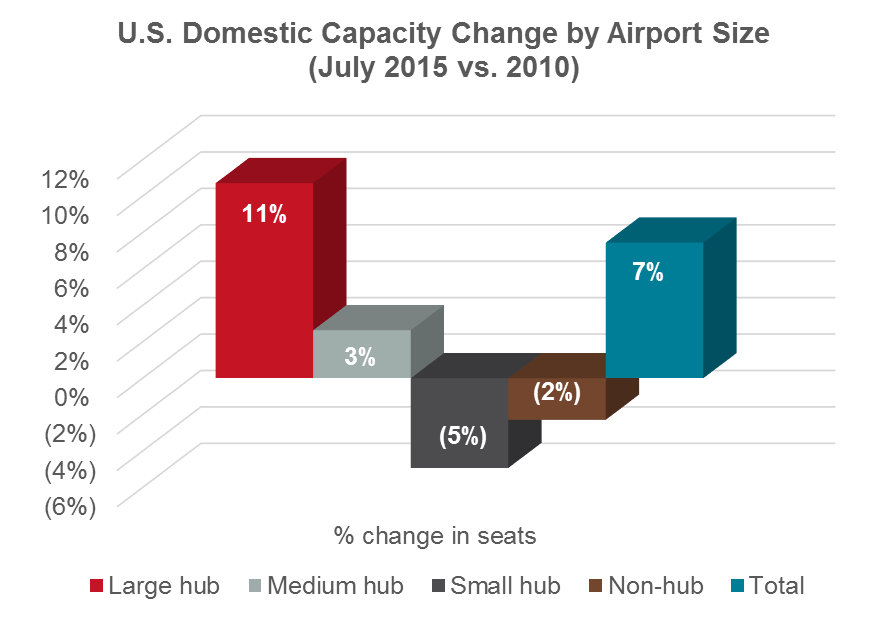

On a national basis, air service has declined double digits since 2008 but has disproportionately affected medium and small hub airports. The figure below demonstrates the change in seat capacity from 2010 to 2015. In their profit improving efforts, traditional network carriers have reduced short-haul flying in favor of long haul and international flying where other transportation alternatives are fewer, time savings are greater, and the profit potential is better.

Changes in the size and type of aircraft (more and larger jets, fewer propeller-driven aircraft) have reduced the number of flights, and these changes have negatively impacted small and mid-size communities to a greater extent. There is a greater opportunity to adjust flight frequency and/or capacity in larger markets to conform to market demand changes than in smaller markets where any adjustment may result in lowering service below marketable levels. Regional hubs (typically medium hub markets) have seen flight frequency reduced, but not necessarily overall capacity because smaller planes have been replaced with larger ones.

Fleet types are changing rapidly in this new industry state as smaller turboprop and regional jet aircraft are being phased out or replaced by larger regional jets and narrow-body jets. Changing fuel costs, demographic changes and aging fleets have forced airlines to replace 50-seat and smaller aircraft that have historically served small communities under the hub-and-spoke system with 70-seat and larger regional jets. Demand for these larger aircraft are far exceeding availability as available capacity has been removed from the marketplace. There is currently no replacement for the 50-seat or smaller aircraft on the horizon with manufacturers showing limited interest due to an internal forecast of low demand for aircraft below 70 seats. There has also been a large churn with older mainline jets being replaced with more fuel efficient newer aircraft.

For a time, carriers reduced frequency, eliminated service, and only very selectively increased service into new markets. More recently, dramatically lower fuel costs have driven increases in flight activity, especially by low-cost, point-to-point carriers like Spirit and Frontier. Representing a countervailing force, a nationwide shortage of pilots has sped up the reduction in the retirement of the smaller aircraft and has been a driver of reducing flying on the smallest aircraft types. This situation was exacerbated as a result of legislation imposed by Congress requiring pilots to have significantly more hours before they can get their airline pilot’s license and imposing additional rest time requirements, which increase the number of pilots needed to fly the same schedules. Going forward, additional loss of frequency or elimination of service is likely, especially in smaller markets. Depending on the market, airports with less than 150,000 enplanements are generally at greater risk for loss of service due to the shift towards larger aircraft with more seats.

The various forces at play will affect communities differently depending on their size. As noted, the pilot shortage and trend towards larger aircraft will most likely have negative effects on the smaller markets, which tend to be served by the hub-and-spoke carriers. Larger markets will see growth from point-to-point carriers and selectively by the major carriers.